1. Introduction to AI in Insurance

Artificial Intelligence (AI) is revolutionizing various industries, and the insurance sector is no exception. The integration of AI technologies, such as ai life insurance and ai insurance, is transforming how insurance companies operate, interact with customers, and manage risks. By leveraging AI, insurers can enhance efficiency, improve customer experiences, and make data-driven decisions.

1.1. Overview of AI in the Insurance Industry

AI encompasses a range of technologies, including machine learning, natural language processing, and predictive analytics. In the insurance industry, these technologies are applied in several ways:

- Claims Processing: AI can automate the claims process, reducing the time and effort required for manual reviews. This leads to faster settlements and improved customer satisfaction, particularly in areas like ai insurance claims.

- Underwriting: AI algorithms analyze vast amounts of data to assess risk more accurately. This allows insurers to make better-informed underwriting decisions and offer personalized policies, including ai underwriting and artificial intelligence underwriting.

- Fraud Detection: AI systems can identify patterns and anomalies in data that may indicate fraudulent activity. This helps insurers mitigate losses and protect their bottom line.

- Customer Service: Chatbots and virtual assistants powered by AI can handle customer inquiries 24/7, providing instant support and freeing up human agents for more complex issues. This is particularly relevant for services like ai insurance near me.

- Risk Assessment: AI tools can analyze historical data and predict future risks, enabling insurers to adjust their policies and pricing accordingly. This is crucial for companies focusing on machine learning in insurance and machine learning in the insurance industry.

1.2. Key Benefits of AI for Insurance Transformation

The adoption of AI in the insurance industry offers several significant benefits:

- Increased Efficiency: Automation of routine tasks reduces operational costs and allows employees to focus on higher-value activities, such as those involved in AI in insurance underwriting.

- Enhanced Customer Experience: AI-driven personalization helps insurers tailor products and services to meet individual customer needs, leading to higher satisfaction and loyalty. This is evident in offerings like ai health insurance and ai car insurance.

- Improved Decision-Making: AI provides insights derived from data analysis, enabling insurers to make informed decisions quickly and accurately.

- Cost Reduction: By streamlining processes and reducing fraud, AI can lead to significant cost savings for insurance companies, particularly through solutions like underwriting ai and insurance underwriting ai.

- Competitive Advantage: Insurers that leverage AI effectively can differentiate themselves in a crowded market, attracting more customers and retaining existing ones. This is especially true for companies like ai united insurance and lemonade ai.

1.3. Rapid Innovation's AI Agent Solutions for Enhanced Insurance Processes

As the insurance landscape grows increasingly complex, integrating AI agents into core operations provides a powerful solution for insurers aiming to streamline workflows, improve customer satisfaction, and enhance fraud detection.

At Rapid Innovation, we specialize in developing AI-driven agents customized for the insurance sector. Our AI agents are capable of automating complex, high-volume tasks like claims processing, risk assessment, and customer support with remarkable efficiency and precision. By leveraging machine learning and natural language processing (NLP), these agents can analyze vast data sources in real-time, provide accurate risk scoring, and instantly identify fraud patterns, giving insurers a proactive edge. Beyond operational efficiency, our AI agents offer highly personalized interactions, guiding customers with tailored policy recommendations and providing seamless support through 24/7 virtual assistance. This not only boosts customer retention but also builds stronger, trust-driven client relationships. With Rapid Innovation’s AI agents, insurance companies are equipped to meet modern demands with agility, accuracy, and a customer-first approach, paving the way for significant ROI and sustainable growth in the AI-empowered insurance era.

At Rapid Innovation, we specialize in implementing AI solutions for fraud detection in insurance sector. Our expertise in AI development and consulting enables us to help clients achieve greater ROI by optimizing their operations and enhancing customer engagement. By partnering with us, insurance companies can harness the full potential of AI to drive transformation and stay ahead in a competitive landscape.

In conclusion, AI is not just a trend but a transformative force in the insurance industry, driving efficiency, enhancing customer experiences, and enabling better risk management. Whether through artificial intelligence in insurance or innovative solutions like zestyai and skywatch ai, the future of insurance is undoubtedly intertwined with AI advancements.

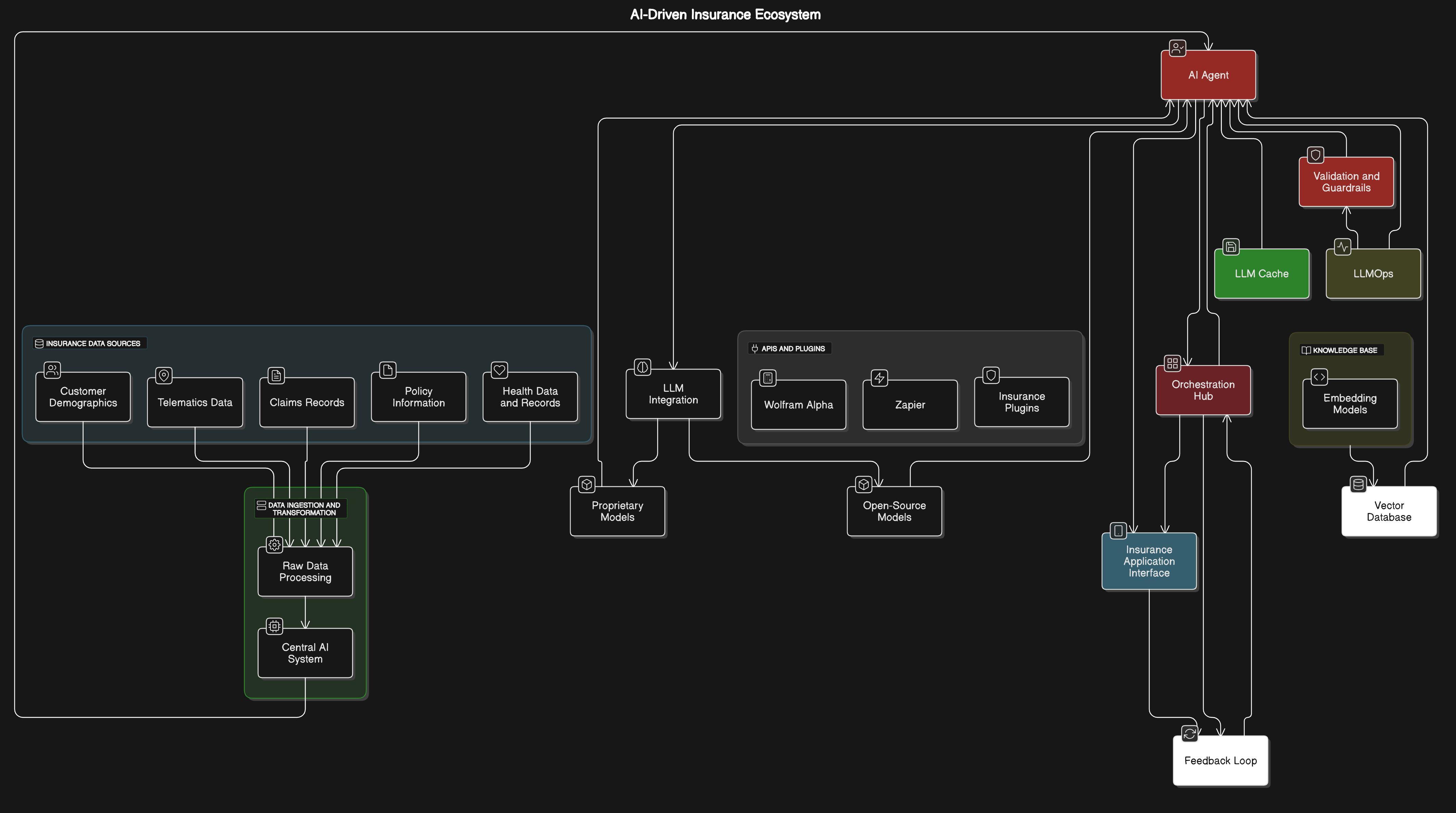

Refer to the image for a visual representation of AI applications in the insurance industry:

2. Claims Processing and Fraud Detection

Claims processing and fraud detection are critical components of the insurance industry. The integration of artificial intelligence (AI) in these areas, such as ai in healthcare claims processing and ai claims processing, has transformed how claims are handled, making the process more efficient and effective.

2.1. AI for Claims Processing – Speeding up Claims Approvals

AI technologies are revolutionizing claims processing by automating various tasks, which leads to faster approvals and improved customer satisfaction. Key advancements include:

- Automated Data Entry: AI can extract information from documents and forms, significantly reducing the need for manual data entry.

- Predictive Analytics: AI algorithms analyze historical data to predict the likelihood of claims being approved, allowing for quicker decision-making.

- Chatbots and Virtual Assistants: These tools provide immediate responses to customer inquiries, guiding them through the claims process and reducing wait times.

- Image Recognition: AI can assess damage through images submitted by claimants, expediting the evaluation process.

- Workflow Automation: AI streamlines the workflow by routing claims to the appropriate adjusters based on complexity and urgency.

The result is a significant reduction in processing time, with some companies reporting a decrease in claims approval time by up to 70%. Rapid Innovation leverages these AI capabilities, including ai for claims processing and ai insurance claims processing, to help clients enhance their operational efficiency and achieve greater ROI.

2.2. AI in Claims Investigation – Streamlining Investigations

AI plays a crucial role in claims investigation, enhancing the ability to detect fraudulent claims and ensuring that legitimate claims are processed efficiently. The main contributions of AI in claim processing include:

- Anomaly Detection: AI systems can analyze patterns in claims data to identify anomalies that may indicate fraud, such as unusual claim amounts or frequency.

- Natural Language Processing (NLP): NLP tools can analyze written statements and communications to detect inconsistencies or red flags in claimant narratives.

- Social Media Monitoring: AI can scan social media platforms for information that may contradict a claimant's statements, providing additional context for investigations.

- Risk Scoring: AI can assign risk scores to claims based on various factors, helping investigators prioritize cases that require deeper scrutiny.

- Historical Data Analysis: By examining past claims and their outcomes, AI can help identify trends and potential fraud schemes, allowing for proactive measures.

These advancements not only improve the accuracy of investigations but also reduce the time spent on each case, leading to more efficient claims handling and a better experience for policyholders. At Rapid Innovation, we harness these AI-driven claim investigation solutions, including machine learning in claims processing and claims automation ai, to empower our clients in the insurance sector, ensuring they can navigate the complexities of claims processing and fraud detection with confidence and agility. For more insights on the future of personalized risk evaluation in insurance with AI agents, visit our website.

Refer to the image for a visual representation of the integration of AI in claims processing and fraud detection in the insurance industry.

2.3. Fraud Detection in Insurance – Identifying and Preventing Fraudulent Claims

Fraud in the insurance industry can lead to significant financial losses. Detecting and preventing fraudulent claims with AI is crucial for maintaining the integrity of insurance operations.

- Types of Insurance Fraud:

- Application Fraud: Providing false information during the application process.

- Claims Fraud: Submitting exaggerated or fabricated claims after an incident.

- Premium Fraud: Misrepresenting information to obtain lower premiums.

- Techniques for Fraud Detection:

- Data Analytics: Utilizing algorithms to analyze patterns in claims data, enabling insurers to identify suspicious activities efficiently. This includes insurance fraud detection and insurance fraud analytics.

- Machine Learning: Implementing models that learn from historical data to identify anomalies, thus enhancing the accuracy of fraud detection, particularly in areas like health insurance fraud detection and life insurance fraud detection.

- Predictive Modeling: Forecasting potential fraud based on past behaviors and trends, allowing for proactive measures in fraud detection in insurance claims.

- Indicators of Fraudulent Claims:

- Inconsistent Information: Discrepancies between the claim and the policyholder's history can signal potential fraud.

- Unusual Claim Patterns: A sudden spike in claims from a particular area or demographic may indicate fraudulent activity, such as auto insurance fraud detection.

- Behavioral Red Flags: Claimants who exhibit suspicious behavior during interviews can be flagged for further investigation.

- Prevention Strategies:

- Employee Training: Educating staff on recognizing signs of fraud to create a vigilant workforce.

- Collaboration with Law Enforcement: Partnering with authorities to investigate suspicious claims, enhancing the overall fraud prevention framework.

- Fraud Hotlines: Establishing anonymous reporting systems for whistleblowers to encourage the reporting of fraudulent activities, including insurance fraud prevention initiatives.

2.4. Voice and Sentiment Analysis in Claims – Assessing Sentiment for Risk Indicators

Voice and sentiment analysis can provide valuable insights into the emotional state of claimants, which can be indicative of potential risks or fraudulent behavior. In claims processing voice and sentiment analysis is playing a vital role, some of the applications and benefits are mentioned below.

- Importance of Voice Analysis:

- Tone and Pitch: Variations in tone can signal stress or deception, providing critical cues during claims processing.

- Speech Patterns: Changes in speech rate or pauses may indicate uncertainty or fabrication, aiding in the assessment of claims.

- Sentiment Analysis Techniques:

- Natural Language Processing (NLP): Analyzing the language used by claimants to assess sentiment, allowing for a deeper understanding of their emotional state.

- Emotion Detection: Identifying specific emotions such as anger, fear, or sadness in voice recordings, which can be indicative of potential fraud.

- Applications in Claims Processing:

- Risk Assessment: Evaluating the emotional state of claimants to determine the likelihood of fraud, enhancing the decision-making process.

- Customer Experience: Enhancing interactions by understanding claimant emotions and addressing concerns, leading to improved customer satisfaction.

- Benefits of Voice and Sentiment Analysis:

- Improved Accuracy: More precise identification of potential fraud, reducing financial losses.

- Enhanced Customer Service: Tailoring responses based on emotional cues, fostering a better relationship with clients.

- Faster Claims Processing: Streamlining the evaluation process by focusing on high-risk claims, ultimately improving operational efficiency.

3. Underwriting and Risk Assessment

Underwriting is a critical process in the insurance industry that involves evaluating the risk of insuring a client and determining appropriate premiums.

- Key Components of Underwriting:

- Risk Evaluation: Assessing the likelihood of a claim being made based on various factors, ensuring informed decision-making.

- Data Collection: Gathering information from applications, medical records, and credit histories to create comprehensive risk profiles.

- Risk Classification: Categorizing applicants into different risk groups to set premiums accordingly, optimizing pricing strategies.

- Factors Influencing Risk Assessment:

- Demographics: Age, gender, and location can impact risk levels, necessitating tailored underwriting approaches.

- Behavioral Data: Driving records, health habits, and lifestyle choices are significant indicators that inform risk evaluations.

- Historical Claims Data: Past claims history can predict future risk, allowing for more accurate underwriting decisions.

- Underwriting Techniques:

- Automated Underwriting Systems: Utilizing technology to streamline the underwriting process, enhancing efficiency and accuracy.

- Risk Scoring Models: Implementing algorithms that assign scores based on risk factors, facilitating data-driven decision-making.

- Expert Underwriting: Involving experienced underwriters for complex cases requiring human judgment, ensuring nuanced evaluations.

- Importance of Accurate Risk Assessment:

- Financial Stability: Ensures the insurer can cover claims without incurring losses, safeguarding the organization's viability.

- Competitive Pricing: Allows for fair premium pricing based on individual risk profiles, enhancing market competitiveness.

- Regulatory Compliance: Adhering to legal standards in underwriting practices, mitigating compliance risks.

- Challenges in Underwriting:

- Data Privacy: Balancing the need for information with privacy concerns, ensuring ethical data usage.

- Evolving Risks: Adapting to new risks such as cyber threats and climate change, necessitating continuous updates to underwriting practices.

- Technological Integration: Ensuring systems work seamlessly with existing processes, optimizing operational workflows.

At Rapid Innovation, we leverage our expertise in AI and Blockchain to enhance these processes, providing tailored solutions that drive efficiency and improve ROI for our clients in the insurance sector. By integrating advanced technologies, we help organizations not only detect and prevent fraud, including insurance claim fraud detection and fraud detection in health insurance, but also streamline underwriting and risk assessment, ultimately leading to better financial outcomes. For more insights, check out our article on generative AI in insurance.

Refer to the image for a visual representation of the fraud detection process in insurance.

3.1. AI for Underwriting – Enhancing Risk Assessment and Accuracy

- AI technologies are transforming the underwriting process in insurance by improving risk assessment and accuracy. Machine learning algorithms analyze vast amounts of data, identifying patterns that human underwriters may overlook, particularly in areas like ai underwriting and underwriting ai.

- Key benefits of AI in underwriting include:

- Faster processing times, allowing insurers to make quicker decisions.

- Enhanced accuracy in risk evaluation, reducing the likelihood of underwriting errors.

- Improved customer experience through streamlined applications and faster approvals.

- AI can assess various data sources, including:

- Social media activity

- Online behavior

- Historical claims data

- By integrating AI, insurers can create more personalized policies tailored to individual risk profiles. The use of artificial intelligence underwriting can lead to more competitive pricing, benefiting both insurers and clients. According to a report, AI reduces underwriting costs by up to 30% (source: McKinsey). At Rapid Innovation, we specialize in implementing AI insurance services that enhance underwriting processes, ensuring our clients achieve greater efficiency and ROI. This includes ai in insurance underwriting and ai for underwriting.

3.2. Risk Scoring in Insurance – Scoring and Categorizing Client Risk Levels

- Risk scoring is a critical component of the insurance industry, helping insurers categorize clients based on their risk levels. Insurers use various factors to determine risk scores, including:

- Credit history

- Claims history

- Demographic information

- The risk scoring process involves:

- Collecting data from multiple sources

- Analyzing the data to assign a score that reflects the likelihood of a claim being made

- Benefits of effective risk scoring include:

- More accurate pricing of insurance policies

- Better identification of high-risk clients

- Enhanced fraud detection capabilities

- Insurers can use risk scores to:

- Tailor coverage options to meet specific client needs

- Implement targeted marketing strategies

- The use of advanced analytics in risk scoring can lead to improved decision-making and reduced losses for insurers. Research indicates that effective risk scoring can improve underwriting accuracy by up to 20% (source: Deloitte). Rapid Innovation provides tailored risk scoring solutions that empower insurers to optimize their pricing strategies and enhance client relationships, including machine learning in insurance underwriting.

3.3. Predictive Analytics in Insurance – Forecasting Trends and Client Needs

- Predictive analytics is revolutionizing the insurance industry by enabling insurers to forecast trends and anticipate client needs. This predictive analytics in insurance utilizes historical data and statistical algorithms to predict future outcomes, such as:

- Claim frequency

- Customer behavior

- Market trends

- Key applications of predictive analytics in insurance include:

- Identifying potential claims before they occur

- Enhancing customer retention strategies by predicting when clients may switch providers

- Optimizing pricing models based on predicted risk levels

- Benefits of predictive analytics include:

- Improved operational efficiency through better resource allocation

- Enhanced customer satisfaction by proactively addressing client needs

- Increased profitability by reducing claim costs and improving underwriting accuracy

- Insurers can leverage predictive analytics to:

- Develop targeted marketing campaigns

- Create personalized insurance products

- Monitor emerging risks in real-time

- Studies show that companies using predictive analytics can achieve a 10-15% increase in profitability (source: PwC). At Rapid Innovation, we harness the power of predictive analytics to help our clients stay ahead of market trends and enhance their decision-making processes, ultimately driving greater ROI. This includes applications of ai in underwriting and machine learning in underwriting.

3.4. AI for Risk Assessment and Management – Assessing and Mitigating Risks

AI technologies are increasingly being utilized in risk assessment and management across various industries. Machine learning algorithms analyze vast amounts of data to identify potential risks and predict future outcomes. Key applications include:

- Financial services: AI assesses credit risk by analyzing customer data and transaction history.

- Healthcare: AI predicts patient risks by analyzing medical records and treatment histories.

- Cybersecurity: AI detects anomalies in network traffic to identify potential security breaches.

The benefits of AI in risk management are significant:

- Enhanced accuracy: AI can process data faster and more accurately than traditional methods.

- Real-time monitoring: Continuous data analysis allows for immediate risk detection and response.

- Cost efficiency: Automating risk assessment reduces the need for extensive human resources.

However, challenges remain:

- Data privacy concerns: Handling sensitive information requires strict compliance with regulations.

- Algorithm bias: AI systems can perpetuate existing biases if not properly managed.

- Integration issues: Incorporating AI into existing risk management frameworks, such as the nist risk management frameworks, can be complex.

Companies leveraging AI for risk management report improved decision-making and reduced losses. At Rapid Innovation, we specialize in implementing AI solutions tailored to your specific industry needs, ensuring that you can navigate risks effectively while maximizing your return on investment. This includes utilizing the nist ai risk management framework and the nist artificial intelligence risk management framework to guide our strategies.

4. Customer Service and Personalization in Insurance

AI is transforming insurance customer service by enabling personalized experiences and efficient interactions. Key features of AI in customer service include:

- Data analysis: AI analyzes customer data to understand preferences and behaviors.

- Predictive analytics: Anticipates customer needs based on historical data.

- Automation: Streamlines processes, reducing wait times and improving service quality.

The benefits of AI-driven customer service are notable:

- Enhanced customer satisfaction: Personalized interactions lead to better customer experiences.

- Increased efficiency: AI can handle multiple inquiries simultaneously, freeing up human agents for complex issues.

- Cost savings: Reduces operational costs by automating routine tasks.

Challenges faced in AI customer service include:

- Maintaining a human touch: Balancing automation with personal interaction is crucial.

- Technical limitations: AI may struggle with complex queries that require nuanced understanding.

- Customer acceptance: Some customers may prefer human interaction over AI solutions.

4.1. AI-Powered Customer Service – Implementing Chatbots and Virtual Assistants

Chatbots and virtual assistants are at the forefront of AI-powered customer service. Key functionalities include:

- 24/7 availability: Chatbots provide round-the-clock support, addressing customer inquiries at any time.

- Instant responses: AI can deliver immediate answers to frequently asked questions.

- Multilingual support: Many chatbots can communicate in multiple languages, catering to diverse customer bases.

The benefits of implementing chatbots and virtual assistants are significant:

- Improved response times: Customers receive quick answers, enhancing their overall experience.

- Scalability: Businesses can handle increased customer inquiries without proportional increases in staff.

- Data collection: Chatbots gather valuable customer insights that can inform business strategies.

Best practices for implementation include:

- Define clear objectives: Understand what you want to achieve with AI customer service.

- Train the AI: Use historical data to train chatbots for better accuracy and relevance.

- Monitor performance: Regularly assess chatbot interactions to identify areas for improvement.

Challenges in chatbot implementation involve:

- Understanding context: Chatbots may struggle with complex or ambiguous queries.

- User frustration: Poorly designed chatbots can lead to customer dissatisfaction.

- Integration with existing systems: Ensuring seamless operation with current customer service platforms is essential.

At Rapid Innovation, we are committed to helping businesses harness the power of AI to enhance customer service and achieve greater operational efficiency, ultimately driving higher ROI. Our expertise also extends to ai risk management, ai risk assessment, and the use of machine learning in risk management to further support our clients' needs.

4.2. Customer Retention with AI – Identifying and Retaining At-Risk Customers

- AI technologies can analyze vast amounts of customer data to identify patterns and behaviors indicative of at-risk customers.

- Predictive analytics can forecast customer churn by evaluating factors such as:

- Customer engagement levels

- Payment history

- Service usage patterns

- Machine learning algorithms can segment customers based on their likelihood to leave, allowing for targeted retention strategies.

- AI-driven tools can automate outreach efforts, sending personalized messages or offers to at-risk customers.

- By utilizing sentiment analysis, companies can gauge customer satisfaction and address issues proactively.

- Implementing AI solutions can lead to significant cost savings, as retaining existing customers is often cheaper than acquiring new ones.

- Companies that effectively use AI for customer retention can see improvements in customer loyalty and lifetime value.

At Rapid Innovation, we leverage these AI capabilities, including retention ai and ai customer retention, to help our clients enhance their customer retention strategies, ultimately driving greater ROI through improved customer loyalty and reduced churn rates. For more insights on how AI impacts insurance policies and prices, check out the impact of AI on your insurance policies and prices.

4.3. AI for Policy Recommendations – Suggesting Policies Based on Client Needs

- AI can analyze individual client data to recommend tailored insurance policies that meet specific needs.

- By assessing factors such as:

- Demographics

- Lifestyle choices

- Previous claims history

- AI systems can provide insights into the most suitable coverage options for clients.

- Natural language processing (NLP) can enhance customer interactions by understanding inquiries and providing relevant policy suggestions.

- AI can also evaluate market trends and competitor offerings to ensure recommendations are competitive and relevant.

- This personalized approach can lead to higher customer satisfaction and increased policy uptake.

- Insurers can leverage AI to streamline the policy recommendation process, reducing the time agents spend on manual assessments.

At Rapid Innovation, we implement AI-driven policy recommendation systems that not only enhance client satisfaction but also optimize operational efficiency, leading to increased profitability for our clients.

4.4. Personalized Insurance Products – Tailoring Offerings Based on Risk Profiles

- AI enables insurers to create personalized insurance products by analyzing individual risk profiles.

- Key factors influencing risk profiles include:

- Age

- Health status

- Driving behavior (for auto insurance)

- Property characteristics (for home insurance)

- By utilizing data from IoT devices, insurers can gain real-time insights into customer behavior and adjust policies accordingly.

- Customization can lead to more accurate pricing, ensuring customers pay for coverage that reflects their actual risk.

- Personalized products can enhance customer engagement, as clients feel their unique needs are being addressed.

- AI can facilitate dynamic pricing models, allowing for adjustments based on changing risk factors over time.

- This approach not only improves customer satisfaction but also helps insurers manage risk more effectively.

At Rapid Innovation, we empower insurers to harness AI for creating personalized insurance products, ensuring that they meet the evolving needs of their clients while maximizing their competitive edge in the market.

5. Document Processing and Natural Language Processing (NLP)

Document processing and Natural Language Processing (NLP) are critical components in the insurance industry, enabling organizations to manage vast amounts of textual data efficiently. These technologies help automate the extraction, analysis, and understanding of information from various documents, such as policies, claims, and contracts.

- Document processing involves the use of software to convert different types of documents into machine-readable formats.

- NLP is a branch of artificial intelligence that focuses on the interaction between computers and human language, allowing machines to understand, interpret, and generate human language.

- Together, these technologies streamline workflows, reduce manual errors, and enhance decision-making processes.

5.1. NLP for Insurance Documents – Processing and Understanding Policies, Claims, and Contracts

NLP in processing insurance documents, is making it easier for companies to handle complex information efficiently.

- Policy Analysis: NLP algorithms can analyze insurance policies to extract key terms, conditions, and coverage details, helping in identifying discrepancies and ensuring compliance with regulations.

- Claims Processing: NLP can automate the extraction of relevant information from claims submissions, such as claimant details, incident descriptions, and supporting documents. This reduces the time taken to process claims and improves customer satisfaction.

- Contract Understanding: NLP tools can assist in reviewing contracts by identifying critical clauses and obligations, ensuring that all parties understand their responsibilities and reducing the risk of disputes.

- Sentiment Analysis: NLP can analyze customer feedback and sentiment from various sources, including social media and surveys. This helps insurers gauge customer satisfaction and identify areas for improvement.

- Risk Assessment: By analyzing historical claims data and policy documents, NLP can help insurers assess risks more accurately, leading to better underwriting decisions and pricing strategies.

At Rapid Innovation, we leverage our expertise in AI and NLP to develop tailored solutions that enhance document processing capabilities for our clients in the insurance sector. By implementing our advanced NLP algorithms, clients can achieve significant improvements in operational efficiency and customer satisfaction, ultimately leading to greater ROI.

6. Specialized AI Applications in Insurance

The insurance industry is increasingly adopting specialized AI applications to enhance operational efficiency, improve customer service, and drive innovation.

- Fraud Detection: AI algorithms can analyze patterns in claims data to identify potential fraudulent activities. Machine learning models can flag suspicious claims for further investigation, reducing losses due to fraud.

- Chatbots and Virtual Assistants: AI-powered chatbots can handle customer inquiries, provide policy information, and assist with claims filing. This improves customer engagement and reduces the workload on human agents.

- Predictive Analytics: AI applications can analyze historical data to predict future trends, such as claim frequency and severity. This enables insurers to make data-driven decisions regarding risk management and pricing.

- Personalized Insurance Products: AI can analyze customer data to create tailored insurance products that meet individual needs, enhancing customer satisfaction and loyalty.

- Automated Underwriting: AI systems can streamline the underwriting process by analyzing applicant data and making real-time decisions. This reduces the time required for policy issuance and improves operational efficiency.

- Telematics and Usage-Based Insurance: AI applications in telematics collect and analyze data from connected devices to assess driving behavior. This allows insurers to offer usage-based insurance policies, rewarding safe driving habits with lower premiums.

- Claims Automation: AI can automate various stages of the claims process, from initial reporting to final settlement, leading to faster claims resolution and improved customer experience.

- Regulatory Compliance: AI tools can help insurers stay compliant with ever-changing regulations by monitoring and analyzing relevant data. This reduces the risk of non-compliance penalties and enhances operational transparency.

At Rapid Innovation, we are committed to helping our clients harness the power of AI to drive innovation and achieve their business goals efficiently and effectively. Our specialized solutions in fraud detection, predictive analytics, and claims automation are designed to deliver measurable results and enhance overall operational performance.

In the context of nlp in insurance, nlp use cases in insurance are becoming increasingly relevant as organizations seek to optimize their processes. The integration of natural language processing in insurance is transforming how companies interact with their clients and manage their operations. As the industry evolves, the importance of nlp insurance will only continue to grow, making it essential for organizations to stay ahead of the curve.

6.1. AI in Life Insurance – Predicting Life Expectancy and Personalizing Plans

AI technologies are transforming the life insurance industry by enabling more accurate predictions of life expectancy. Machine learning algorithms analyze vast amounts of data, including:

- Medical history

- Lifestyle choices (e.g., smoking, exercise)

- Genetic information

These insights allow insurers to:

- Offer personalized insurance plans tailored to individual risk profiles.

- Adjust premiums based on predicted life expectancy, making policies more equitable.

AI can also enhance customer experience by:

- Providing real-time feedback on health and wellness.

- Offering personalized recommendations for improving life expectancy.

Insurers can leverage AI to identify trends and patterns in mortality rates, leading to better risk management. The use of AI in underwriting processes can reduce the time taken to assess applications, improving efficiency. Companies like Prudential and John Hancock are already utilizing AI to refine their underwriting processes and enhance customer engagement. At Rapid Innovation, we specialize in developing AI insurance solutions that empower life insurance companies, including ai life insurance and ai insurance, to harness these capabilities, ultimately driving greater ROI through improved customer satisfaction and operational efficiency.

6.2. AI for Health Insurance – Enhancing Claims Processing and Personalization

AI is revolutionizing health insurance by streamlining claims processing and improving personalization. Automated systems powered by AI can:

- Analyze claims data quickly and accurately.

- Detect fraudulent claims through pattern recognition.

This leads to:

- Reduced processing times, allowing for faster reimbursements.

- Lower operational costs for insurers.

AI can also personalize health insurance plans by:

- Analyzing individual health data to recommend tailored coverage options.

- Offering preventive care suggestions based on predictive analytics.

Insurers can use AI to monitor patient health trends, leading to proactive interventions. Chatbots and virtual assistants powered by AI enhance customer service by:

- Providing instant responses to inquiries.

- Assisting with claims submissions and tracking.

Companies like Anthem and UnitedHealth Group are leveraging AI to improve their claims processing and customer engagement strategies. Rapid Innovation can assist health insurers in implementing these AI-driven solutions, ensuring they achieve significant cost savings and improved service delivery, including ai insurance near me and ai united insurance near me.

6.3. Telematics and AI in Auto Insurance – Adjusting Rates Using Telematics Data

Telematics technology, combined with AI, is reshaping the auto insurance landscape. Insurers collect data from telematics devices installed in vehicles, which track:

- Driving behavior (e.g., speed, braking patterns)

- Vehicle location

- Time of day driving occurs

AI analyzes this data to:

- Assess risk more accurately and adjust premiums accordingly.

- Identify safe drivers and reward them with discounts.

This data-driven approach leads to:

- More personalized insurance rates based on actual driving behavior rather than demographic factors.

- Enhanced safety features, as insurers can provide feedback to drivers on their habits.

Telematics can also assist in accident detection and reporting, leading to:

- Faster claims processing.

- Improved customer satisfaction.

Companies like Progressive and Allstate are at the forefront of integrating telematics and AI to refine their pricing models and enhance customer experiences. Rapid Innovation offers expertise in developing telematics solutions that not only optimize pricing strategies but also enhance overall customer engagement, driving higher returns on investment for auto insurers, including ai car insurance and ai auto insurance.

6.4. Computer Vision for Property and Casualty Insurance – Assessing Property Damage

Computer vision technology is revolutionizing the way property and casualty insurance companies assess damage. By utilizing advanced algorithms and machine learning, insurers can analyze images and videos to determine the extent of property damage more efficiently and accurately.

- Automated Damage Assessment

Computer vision can automatically identify and classify damage in images, significantly reducing the time needed for manual inspections and expediting the claims process. - Enhanced Accuracy

Algorithms can detect subtle damage that might be overlooked by human adjusters, leading to more precise assessments and fairer settlements for policyholders. - Cost Efficiency

This technology minimizes the need for on-site inspections, saving both time and resources. Insurers can process claims faster, thereby improving customer satisfaction. - Real-Time Analysis

Insurers can analyze damage as soon as images are uploaded, facilitating quicker decision-making. This capability is particularly beneficial in disaster scenarios where timely responses are critical. - Integration with Drones

Drones equipped with cameras can capture aerial images of properties. Computer vision can analyze these images to assess damage in hard-to-reach areas, enhancing the thoroughness of evaluations. - Fraud Detection

Advanced algorithms can identify inconsistencies in claims, aiding in the detection of fraudulent activities. This protects insurers from losses and ensures that legitimate claims are processed efficiently.

7. Advanced Insurance Pricing and Actuarial Models

Advanced insurance pricing and actuarial models are essential for insurance companies to remain competitive and financially stable. These insurance pricing models leverage data analytics and statistical techniques to set premiums that accurately reflect the risk associated with insuring a particular individual or property.

- Data-Driven Insights

Insurers utilize vast amounts of data, including historical claims, customer demographics, and market trends. This data is crucial for understanding risk factors and predicting future claims. - Predictive Analytics

Advanced models employ predictive analytics to forecast potential losses, enabling insurers to proactively adjust pricing strategies. - Risk Segmentation

Insurers can segment customers based on risk profiles, leading to more tailored pricing. This ensures that low-risk customers are not overcharged while high-risk customers pay appropriately. - Regulatory Compliance

Advanced models assist insurers in complying with regulatory requirements regarding pricing fairness, which is vital for maintaining trust and transparency with customers. - Continuous Improvement

Insurers can continuously refine their models based on new data and changing market conditions. This adaptability is essential in a rapidly evolving insurance landscape.

7.1. AI-Powered Pricing Models – Creating Dynamic and Fair Pricing Structures

AI-powered pricing models are transforming how insurance companies determine premiums. By incorporating artificial intelligence, insurers can create dynamic pricing structures that are both fair and competitive.

- Real-Time Data Utilization

AI models can analyze real-time data from various sources, including social media, IoT devices, and market trends. This capability allows for immediate adjustments to pricing based on current risk factors. - Personalized Pricing

AI enables insurers to offer personalized premiums based on individual behavior and risk profiles, fostering customer loyalty and satisfaction. - Enhanced Risk Assessment

Machine learning algorithms can identify patterns in data that traditional models may overlook, leading to more accurate risk assessments and pricing. - Competitive Advantage

Insurers utilizing AI-powered models can respond more swiftly to market changes and customer needs. This agility provides a significant edge over competitors. - Improved Customer Experience

Dynamic pricing models can offer customers more options and transparency in their premiums, enhancing the overall customer experience and building trust. - Ethical Considerations

Insurers must ensure that AI models are free from bias and discrimination. Fair pricing practices are essential to maintain regulatory compliance and customer trust.

At Rapid Innovation, we leverage our expertise in AI and blockchain technologies to help insurance companies implement these advanced solutions. By integrating computer vision, including vsp computer vision care, and AI-powered pricing models, we enable our clients to achieve greater efficiency, accuracy, and customer satisfaction, ultimately driving higher ROI. Our tailored consulting services ensure that your organization can navigate the complexities of these technologies and harness their full potential for business growth. Additionally, we assist in developing blockchain insurance solutions that align with industry standards and customer needs. Moreover, we explore how artificial intelligence is reshaping price optimization to enhance pricing strategies in the insurance sector.

7.2. Predictive Maintenance for Insurers – Forecasting Failures for Equipment/Property

Predictive maintenance is a proactive approach that utilizes data analysis to forecast when equipment or property is likely to fail. This method is particularly advantageous for insurers, as it aids in minimizing losses and enhancing customer satisfaction.

- Utilizes data from IoT devices and sensors to monitor equipment health.

- Analyzes historical data to identify patterns and predict future failures.

- Reduces downtime by scheduling maintenance before failures occur.

- Enhances risk assessment by providing insights into the condition of insured assets.

- Helps insurers offer tailored policies based on the actual risk profile of the equipment or property.

- Can lead to cost savings by preventing catastrophic failures and associated claims.

- Supports better resource allocation by optimizing maintenance schedules.

7.3. Enhanced Actuarial Models – Improving Predictions with AI-Driven Data Models

The integration of artificial intelligence (AI) into actuarial models is revolutionizing the insurance industry. AI-driven data models enhance the accuracy of predictions and improve decision-making processes.

- Leverages machine learning algorithms to analyze vast amounts of data.

- Identifies complex patterns that traditional models may overlook.

- Improves risk assessment by incorporating diverse data sources, including social media and economic indicators.

- Enables real-time data processing, allowing for dynamic pricing and underwriting.

- Enhances fraud detection by recognizing unusual patterns in claims data.

- Facilitates personalized insurance products tailored to individual customer needs.

- Increases operational efficiency by automating routine tasks and reducing manual errors.

8. Compliance and Reinsurance Operations

Compliance and reinsurance operations are critical components of the insurance industry, ensuring that insurers adhere to regulations and manage risk effectively.

- Compliance involves adhering to laws and regulations set by governing bodies.

- Insurers must maintain transparency in their operations and reporting.

- Reinsurance helps insurers mitigate risk by transferring portions of their risk portfolios to other parties.

- Effective compliance management reduces the risk of penalties and enhances reputation.

- Technology plays a vital role in streamlining compliance processes through automation and data analytics.

- Reinsurance operations can be optimized using predictive analytics to assess risk exposure.

- Collaboration with reinsurers can lead to better risk-sharing strategies and improved financial stability.

At Rapid Innovation, we leverage our expertise in AI and blockchain technologies to empower insurers in these areas. By implementing predictive maintenance for insurers, we help clients reduce operational costs and enhance customer satisfaction. Our AI-driven actuarial models enable insurers to make data-informed decisions, improving risk assessment and operational efficiency. Additionally, our blockchain solutions ensure compliance and transparency in reinsurance operations, fostering trust and collaboration within the industry. Through these innovative approaches, Rapid Innovation is committed to helping clients achieve greater ROI and meet their business goals effectively.

8.1. Automation in Insurance Compliance – Ensuring Regulatory Adherence

- Regulatory compliance is crucial for insurance companies to avoid penalties and maintain their licenses.

- Automation tools help streamline compliance processes by:

- Reducing manual data entry and human error.

- Ensuring timely reporting to regulatory bodies.

- Keeping track of changing regulations and standards.

- Key benefits of automation in compliance include:

- Increased efficiency in monitoring compliance activities.

- Enhanced data accuracy and integrity.

- Improved audit trails for regulatory reviews.

- Technologies used in automation:

- Robotic Process Automation (RPA) for repetitive tasks.

- Machine learning algorithms to analyze compliance data.

- Blockchain for secure and transparent record-keeping.

- Companies adopting automation in insurance compliance can expect:

- Cost savings from reduced labor and error correction.

- Faster response times to regulatory changes.

- Better risk management through proactive compliance monitoring.

At Rapid Innovation, we leverage these automation tools to help our clients in the insurance sector enhance their compliance processes, ensuring they remain ahead of regulatory changes while minimizing operational costs. For more insights on the role of automation in various sectors, check out our article on generative AI in finance and banking applications.

8.2. AI in Reinsurance – Streamlining Underwriting and Claims for Reinsurance

- Reinsurance plays a critical role in the insurance industry by providing risk management solutions.

- AI technologies are transforming reinsurance by:

- Enhancing underwriting processes through predictive analytics.

- Automating claims processing to reduce turnaround times.

- Benefits of AI in reinsurance include:

- Improved risk assessment using vast datasets.

- Faster decision-making in underwriting and claims approval.

- Enhanced customer experience through quicker responses.

- Key applications of AI in reinsurance:

- Natural Language Processing (NLP) for analyzing policy documents and claims.

- Machine learning models to predict loss events and trends.

- Chatbots for customer service and claims inquiries.

- The integration of AI can lead to:

- More accurate pricing models.

- Increased profitability through better risk selection.

- Greater operational efficiency and reduced costs.

Rapid Innovation specializes in implementing AI solutions that streamline underwriting and claims processes, enabling our clients to achieve greater profitability and improved customer satisfaction.

9. AI for Disaster Risk Management

- Disaster risk management is essential for minimizing the impact of natural disasters on communities and economies.

- AI technologies are being utilized to enhance disaster preparedness and response by:

- Analyzing historical data to predict future disaster events.

- Utilizing satellite imagery and sensors for real-time monitoring.

- Key benefits of AI in disaster risk management include:

- Improved accuracy in risk assessments and hazard mapping.

- Faster response times during emergencies through automated alerts.

- Enhanced resource allocation based on predictive analytics.

- Applications of AI in disaster risk management:

- Machine learning algorithms for modeling disaster scenarios.

- Drones and AI-powered imaging for damage assessment.

- Social media analysis to gauge public sentiment and needs during disasters.

- The impact of AI on disaster risk management can lead to:

- Reduced loss of life and property.

- More resilient communities through better preparedness.

- Increased collaboration among agencies and organizations for effective response.

At Rapid Innovation, we harness AI technologies to empower organizations in disaster risk management, ensuring they are better prepared and equipped to respond effectively to emergencies. Our solutions not only enhance operational efficiency but also contribute to the safety and resilience of communities.

9.1. Predicting Natural Disasters – Using AI for Proactive Disaster Management

Artificial Intelligence (AI) is revolutionizing the way we predict and manage natural disasters. By analyzing vast amounts of data, AI can identify patterns and trends that may indicate an impending disaster.

- Machine Learning Algorithms: These algorithms can process historical data on weather patterns, seismic activity, and other environmental factors to predict events like hurricanes, earthquakes, and floods. Rapid Innovation leverages these algorithms to provide clients with tailored predictive models that enhance their disaster preparedness strategies.

- Real-time Data Analysis: AI systems can analyze real-time data from satellites, sensors, and social media to provide timely alerts and updates. Our solutions enable organizations to receive immediate insights, allowing for swift decision-making during critical situations.

- Enhanced Accuracy: AI models can improve prediction accuracy by continuously learning from new data, reducing false alarms and increasing public trust in warnings. Rapid Innovation's expertise in AI ensures that clients benefit from cutting-edge models that adapt to evolving data landscapes.

- Risk Assessment: AI can help assess the vulnerability of different regions, allowing for targeted preparedness efforts and resource allocation. We assist clients in developing comprehensive risk assessment frameworks that prioritize resource deployment effectively.

- Case Studies: Various organizations, such as the National Oceanic and Atmospheric Administration (NOAA), are using AI to enhance their forecasting capabilities, leading to better disaster preparedness. Rapid Innovation collaborates with similar entities to implement AI-driven solutions that optimize their operational efficiency. For more insights, check out our post on learning from real-world AI implementations.

9.2. Risk Mitigation Strategies – Preparing for and Responding to Disasters

Effective risk mitigation strategies are essential for minimizing the impact of natural disasters. These strategies involve both preparation and response measures.

- Emergency Preparedness Plans: Developing comprehensive plans that outline roles, responsibilities, and procedures for various disaster scenarios. Rapid Innovation helps organizations create robust plans that ensure readiness for any eventuality.

- Community Training: Conducting training sessions and drills for community members to ensure they know how to respond during a disaster. Our training programs are designed to empower communities with the knowledge and skills necessary for effective disaster response.

- Infrastructure Resilience: Investing in infrastructure improvements, such as flood barriers and earthquake-resistant buildings, to withstand natural disasters. We provide consulting services to help clients identify and implement necessary infrastructure enhancements.

- Early Warning Systems: Implementing systems that provide timely alerts to communities at risk, allowing them to evacuate or take protective measures. Rapid Innovation specializes in developing advanced early warning systems that integrate AI for real-time monitoring.

- Collaboration: Engaging with local governments, NGOs, and community organizations to create a coordinated response plan that leverages resources and expertise. We facilitate partnerships that enhance collective disaster response capabilities.

- Post-Disaster Recovery: Establishing protocols for recovery efforts, including mental health support and rebuilding initiatives, to help communities bounce back after a disaster. Our expertise extends to developing comprehensive recovery strategies that prioritize community well-being.

10. ROI Calculator for AI in Insurance

The integration of AI in the insurance industry has the potential to significantly enhance operational efficiency and customer satisfaction. An ROI calculator can help insurance companies assess the financial benefits of implementing AI technologies.

- Cost Savings: AI can automate routine tasks, reducing labor costs and minimizing human error. Rapid Innovation's AI solutions streamline operations, leading to substantial cost reductions for our clients.

- Improved Underwriting: AI algorithms can analyze data more accurately, leading to better risk assessment and pricing strategies. We empower insurers with advanced analytics tools that enhance their underwriting processes.

- Enhanced Customer Experience: AI-driven chatbots and virtual assistants can provide 24/7 support, improving customer engagement and satisfaction. Our AI solutions are designed to elevate customer interactions, fostering loyalty and retention.

- Fraud Detection: AI can identify suspicious patterns in claims data, helping to reduce fraudulent claims and associated costs. Rapid Innovation implements sophisticated fraud detection systems that safeguard our clients' interests.

- Data-Driven Insights: AI can provide actionable insights from data analytics, enabling insurers to make informed decisions and optimize their operations. We equip clients with the analytical capabilities needed to drive strategic initiatives.

- Customization: AI allows for personalized insurance products based on individual customer data, leading to higher retention rates and customer loyalty. Our solutions enable insurers to tailor offerings that meet the unique needs of their clientele, enhancing overall satisfaction.

Incorporating AI in disaster management and insurance not only enhances predictive capabilities but also fosters proactive disaster management strategies that can save lives and resources. For more information on how we can assist you, visit our AI consulting services.

11. Frequently Asked Questions (FAQ)

11.1. What is the potential ROI of implementing AI in insurance?

The potential return on investment (ROI) from implementing AI in the insurance sector can be significant. Here are some key points to consider:

- Cost Reduction: AI can automate routine tasks, reducing the need for manual labor and minimizing operational costs. This can lead to savings in administrative expenses.

- Improved Accuracy: AI algorithms can analyze vast amounts of data with high precision, reducing errors in underwriting and claims processing. This can lead to fewer losses and better risk management.

- Enhanced Customer Experience: AI-driven chatbots and virtual assistants can provide 24/7 customer support, improving customer satisfaction and retention rates. Happy customers are more likely to renew policies and recommend services.

- Faster Decision-Making: AI can process data and generate insights quickly, allowing insurers to make faster decisions regarding underwriting and claims. This speed can lead to a competitive advantage in the market.

- Fraud Detection: AI can identify patterns and anomalies in data that may indicate fraudulent activity, potentially saving insurers millions in fraudulent claims. According to a report, AI can reduce fraud by up to 50% in some cases.

- Market Growth: By leveraging AI, insurers can develop new products and services tailored to customer needs, opening up new revenue streams. The global AI in insurance market is projected to grow significantly, indicating a strong potential for ROI. This includes innovations like ai life insurance and ai insurance industry solutions.

11.2. How does AI improve claims processing efficiency?

AI enhances claims processing efficiency through various innovative approaches. Here are some ways it achieves this:

- Automation of Routine Tasks: AI can automate repetitive tasks such as data entry, document verification, and initial claim assessments, freeing up human resources for more complex tasks.

- Data Analysis: AI systems can analyze large volumes of claims data quickly, identifying trends and patterns that can streamline the claims process. This leads to faster claim resolutions, particularly in areas like ai underwriting.

- Predictive Analytics: AI can use historical data to predict claim outcomes, helping insurers to prioritize claims that are likely to be straightforward and expedite their processing.

- Natural Language Processing (NLP): AI can utilize NLP to understand and process claims submitted in natural language, making it easier to assess claims without extensive manual review.

- Fraud Detection: AI algorithms can flag suspicious claims for further investigation, reducing the time spent on fraudulent claims and allowing legitimate claims to be processed more quickly.

- Customer Communication: AI-powered chatbots can handle customer inquiries regarding claims status, providing real-time updates and reducing the workload on customer service representatives. This is particularly useful for services like ai insurance near me.

- Integration with Other Technologies: AI can work alongside other technologies, such as blockchain and IoT, to enhance data sharing and transparency in the claims process, further improving efficiency.

At Rapid Innovation, we specialize in implementing AI solutions tailored to the insurance industry, including Generative AI insurance solutions, ai auto insurance and artificial intelligence in insurance, ensuring that our clients achieve optimal ROI while enhancing operational efficiency and customer satisfaction.

11.3. Can AI completely eliminate fraud in insurance claims?

- AI has the potential to significantly reduce fraud in insurance claims but may not completely eliminate it.

- Fraud detection systems powered by AI insurance claims can analyze vast amounts of data quickly, identifying patterns and anomalies that may indicate fraudulent activity.

- Machine learning algorithms can learn from historical claims data, improving their ability to detect suspicious claims over time, particularly in the context of machine learning in insurance claims.

- AI can flag claims for further investigation, allowing human adjusters to focus on high-risk cases. This targeted approach not only enhances efficiency but also optimizes resource allocation, leading to greater ROI for insurance companies.

- However, fraudsters are also becoming more sophisticated, using technology to create more convincing fraudulent claims, which is a challenge for AI in claims processing.

- The dynamic nature of fraud means that while AI can reduce the incidence of fraud, it cannot eradicate it entirely.

- Continuous updates and training of AI systems are necessary to keep pace with evolving fraud tactics, ensuring that the systems remain effective and relevant.

- Human oversight remains crucial, as AI may not always understand the context or nuances of certain claims. This collaboration between AI and human expertise can lead to more informed decision-making and improved outcomes.

11.4. How does AI enhance underwriting accuracy?

- AI enhances underwriting accuracy by providing data-driven insights that improve decision-making.

- Predictive analytics can assess risk more effectively by analyzing a wide range of data sources, including historical claims data, customer behavior patterns, and external data such as credit scores and social media activity.

- AI algorithms can identify correlations and trends that human underwriters might overlook, leading to more precise risk assessments.

- Automation of data collection and analysis speeds up the underwriting process, allowing for quicker decisions and reducing operational costs.

- AI can help in segmenting customers more accurately, leading to tailored insurance products and pricing that meet specific customer needs, ultimately enhancing customer satisfaction and retention.

- Continuous learning from new data allows AI systems to adapt and refine their models, improving accuracy over time. This adaptability can lead to a more competitive edge in the market.

- Enhanced accuracy in underwriting can lead to better risk management and reduced loss ratios for insurance companies, translating into higher profitability and ROI.

11.5. What are the challenges of integrating AI in insurance?

- Data quality and availability are significant challenges; AI systems require large amounts of high-quality data to function effectively.

- Legacy systems in many insurance companies may not be compatible with modern AI technologies, leading to integration issues that can hinder operational efficiency.

- There is a need for skilled personnel who can manage and interpret AI systems, which may be in short supply, creating a bottleneck in implementation.

- Regulatory compliance is a concern, as insurance is a heavily regulated industry, and AI applications must adhere to various laws and guidelines to avoid legal repercussions.

- Ethical considerations arise, particularly regarding data privacy and the potential for bias in AI algorithms, which can impact customer trust and brand reputation.

- Resistance to change within organizations can hinder the adoption of AI technologies, as employees may be wary of job displacement or changes in workflow.

- The cost of implementing AI solutions can be high, especially for smaller insurance companies with limited budgets, making it essential to demonstrate clear ROI to stakeholders.

- Continuous monitoring and updating of AI systems are necessary to ensure they remain effective and relevant in a rapidly changing environment, requiring ongoing investment and commitment.

At Rapid Innovation, we understand these challenges and are equipped to provide tailored AI and Blockchain solutions that help insurance companies navigate these complexities, ultimately driving efficiency and enhancing ROI, particularly in areas like AI for claims processing and claims automation.

11.6. How does predictive analytics help insurers stay competitive?

Predictive analytics is a powerful tool that enables insurers to analyze historical data and forecast future trends. This capability is crucial for maintaining a competitive edge in the insurance industry.

- Risk assessment: Insurers can better evaluate the risk associated with potential clients, leading to more accurate pricing of policies. Rapid Innovation leverages advanced predictive analytics models to help insurers refine their risk assessment processes, ultimately enhancing profitability. This is particularly relevant in areas such as insurance predictive modeling and predictive analytics in insurance underwriting.

- Fraud detection: Predictive models can identify patterns indicative of fraudulent claims, allowing insurers to take preventive measures. Our expertise in AI-driven fraud detection solutions empowers insurers to minimize losses and improve their bottom line. Claims predictive analytics plays a significant role in this process.

- Customer segmentation: By analyzing customer data, insurers can segment their market and tailor products to meet specific needs, enhancing customer satisfaction. Rapid Innovation assists clients in developing sophisticated segmentation strategies that drive targeted marketing efforts, including predictive analytics for insurance companies.

- Claims management: Predictive analytics can streamline the claims process by anticipating claim volumes and identifying potential bottlenecks. Our solutions help insurers optimize their claims workflows, resulting in faster resolution times and improved customer experiences. This is evident in claims predictive modeling and predictive analytics insurance case studies.

- Marketing strategies: Insurers can optimize their marketing efforts by predicting which customers are most likely to purchase specific products, improving conversion rates. Rapid Innovation's data-driven marketing solutions enable insurers to enhance their outreach and engagement strategies, including predictive analytics health insurance and insurance predictive analytics examples. Additionally, our expertise in Natural Language Processing solutions can further enhance these strategies by analyzing customer interactions and preferences.

11.7. How can AI improve customer experience in insurance?

Artificial Intelligence (AI) is transforming the insurance landscape by enhancing customer interactions and streamlining processes.

- Chatbots and virtual assistants: AI-powered chatbots provide 24/7 customer support, answering queries and guiding users through policy options. Rapid Innovation develops customized chatbot solutions that improve customer engagement and satisfaction.

- Personalized recommendations: AI algorithms analyze customer data to offer tailored insurance products, improving relevance and customer satisfaction. Our AI solutions help insurers deliver personalized experiences that resonate with their clients.

- Claims processing: AI can automate claims assessments, reducing processing time and improving the overall customer experience. Rapid Innovation's AI-driven claims processing tools enhance efficiency and accuracy, leading to quicker payouts.

- Predictive customer service: AI can anticipate customer needs based on historical data, allowing insurers to proactively address issues before they arise. Our predictive analytics capabilities enable insurers to stay ahead of customer expectations.

- Enhanced underwriting: AI can analyze vast amounts of data quickly, leading to faster and more accurate underwriting decisions. Rapid Innovation's AI solutions streamline the underwriting process, reducing time-to-quote and improving risk evaluation.

11.8. What is NLP, and how does it benefit insurance companies?

Natural Language Processing (NLP) is a branch of artificial intelligence that focuses on the interaction between computers and human language. In the insurance sector, NLP offers several advantages.

- Improved customer interactions: NLP enables insurers to analyze customer communications, helping to identify sentiment and improve service quality. Rapid Innovation's NLP solutions enhance customer engagement by providing insights into customer sentiment.

- Automated document processing: NLP can extract relevant information from policy documents and claims, streamlining administrative tasks and reducing manual errors. Our NLP tools help insurers automate document workflows, increasing operational efficiency.

- Enhanced data analysis: Insurers can leverage NLP to analyze unstructured data, such as social media posts and customer reviews, gaining insights into market trends and customer preferences. Rapid Innovation assists clients in harnessing NLP for comprehensive data analysis.

- Fraud detection: NLP can help identify inconsistencies in claims narratives, flagging potential fraud for further investigation. Our NLP-driven fraud detection solutions empower insurers to mitigate risks effectively.

- Regulatory compliance: NLP tools can assist insurers in monitoring communications and documentation to ensure compliance with industry regulations. Rapid Innovation's compliance solutions leverage NLP to help insurers navigate regulatory landscapes seamlessly.

11.9. How is AI used for personalized insurance products?

- AI enables insurers to analyze vast amounts of data to tailor products to individual needs, enhancing customer satisfaction and retention.

- Machine learning algorithms assess customer behavior, preferences, and risk profiles, allowing for more informed decision-making.

- Key applications include:

- Customized policy recommendations based on user data, ensuring that clients receive the most relevant options, such as ai life insurance or ai car insurance.

- Dynamic pricing models that adjust premiums based on real-time data, optimizing profitability while remaining competitive.

- Enhanced customer engagement through personalized communication and offers, fostering stronger relationships with clients.

- AI-driven chatbots provide 24/7 support, answering queries and guiding customers through policy options, which improves service efficiency.

- Predictive analytics help insurers anticipate customer needs and adjust offerings accordingly, leading to increased sales opportunities.

- Insurers can leverage social media and online behavior data to refine their understanding of customer preferences, driving targeted marketing efforts, including ai insurance and artificial intelligence in insurance.

11.10. What is the role of AI in disaster risk management for insurers?

- AI plays a crucial role in assessing and mitigating risks associated with natural disasters, ultimately protecting both insurers and policyholders.

- Key functions include:

- Predictive modeling to forecast potential disaster impacts on insured properties, allowing for proactive risk management.

- Real-time data analysis from various sources (satellite imagery, weather forecasts) to assess risk levels, enhancing situational awareness.

- Automated claims processing during disasters, speeding up response times for affected customers, which improves customer satisfaction.

- AI helps in:

- Identifying high-risk areas for targeted insurance products, enabling insurers to tailor their offerings effectively, such as ai auto insurance.

- Developing risk mitigation strategies by analyzing historical data and trends, which can lead to more resilient business practices.

- Enhancing communication with policyholders during disaster events through automated alerts and updates, ensuring timely information dissemination.

- Insurers can use AI to optimize their reinsurance strategies by better understanding risk exposure, ultimately leading to improved financial stability.

11.11. How does AI assist in regulatory compliance for insurers?

- AI streamlines compliance processes by automating data collection and reporting, reducing operational burdens.

- Key benefits include:

- Enhanced accuracy in regulatory reporting, reducing the risk of human error and potential penalties.

- Continuous monitoring of transactions and activities to detect anomalies or compliance breaches, ensuring adherence to regulations.

- AI tools can:

- Analyze regulatory changes and assess their impact on existing policies and practices, keeping insurers up-to-date.

- Facilitate risk assessments by identifying areas of non-compliance, allowing for timely corrective actions.

- Natural language processing (NLP) helps in interpreting complex regulations and ensuring adherence, simplifying compliance efforts.

- Insurers can leverage AI to maintain comprehensive audit trails, simplifying the compliance verification process and enhancing transparency.

- By automating routine compliance tasks, AI allows insurers to focus on strategic initiatives and customer service, ultimately driving greater ROI and operational efficiency.

At Rapid Innovation, we harness the power of AI technologies to help our clients achieve their business goals efficiently and effectively. By implementing tailored AI insurance solutions, such as ai insurance company and ai underwriting, we enable insurers to enhance customer experiences, optimize risk management, and ensure regulatory compliance, leading to greater returns on investment.